Tax World Reacts

“The Budget 2024 signals the next generation reforms for Viksit Bharat. The Budget proposal announced comes at the backdrop of India’s sustained growth, which carries a tag of fastest growing large emerging economy in the world. A detailed roadmap for the pursuit of its visions covers 9 priorities including agriculture, manufacturing, energy, infrastructure and employments.

On the taxation front, the proposals have recognised the success of introduction of GST leading to buoyancy in collections, broadening of tax base and reduced compliances. Simplification & rationalisation of the GST tax structure is likely to continue as part of the GST Councils agenda. In a welcome step, the Budget proclaimed a comprehensive review of the customs duty rate structure over the next six months, with an aim to rationalise, enhance domestic manufacturing and mitigate disputes.

A slew of measures is proposed to mitigate tax disputes and settle litigation. It includes a comprehensive review of the extant 1961 law and announcement for simplification of reassessment regime including transfer pricing assessments. It has been proposed to reduce the reopening of assessments upto 5 years if income escaped is more than Rs.50 lacs. For search cases, the reopening of assessment has been proposed to be reduced to 6 years from existing 10 years. Further, Vivad Se Vishwas Scheme 2024 has been announced for settling income tax disputes pending in appeal. This is also coupled with increase in monetary limit for filing of appeals to Tribunals, High Courts and Supreme Courts by the tax authorities.

One of the major demands of the start-up ecosystem was removal of the ‘Angel Tax’, the Budget 2024 has announced abolishing of the ‘Angel Tax’, giving much needed relief to entrepreneurial climate. The Finance Minister seems to have delivered a well-balanced Budget, which continues to aim at fiscal consolidation, growth and reforms.”

Budget 2024 -25: Roadmap to Viksit Bharat and adherence to Fiscal Prudence

Continuing the pursuit of 'Viksit Bharat', the budget primarily focuses on 9 key themes including urban development as well as innovation and research whilst laying out and ensuring a fiscal consolidation roadmap.

In respect of personal taxation, the budget promotes the adoption of the new tax regime by revising the slab rates resulting in potential tax savings of up to INR 17,500. Further, increase in the standard deduction by INR 25,000 coupled with additional deduction of INR 10,000 on family pension would lead to higher disposable incomes in the hands of the individuals.

On the corporate taxes front, the popular expectation of extension of the sunset clause beyond 31st March 2024 for eligible manufacturing units registered under section 115BAB was not met. Further, the budget abolished the buy back tax starting 01st October 2024 post which the buy back proceeds would be taxed as dividends in the hands of the shareholders with the corresponding cost being available for carry forward and set-off against future capital gains.

The much talked about capital gain rationalisation found its place in the Budget in the following manner:

The exemption in respect of securities covered under section 112A has been increased from INR 1,00,000 to INR 1,25,000.

Also, the ambiguities surrounding taxability of corporate gifts was put to rest by restricting the gift exemption to individuals and HUFs.

With the intent to give further momentum to foreign direct investments the FDI and ODI regimes are proposed to be simplified and the corporate tax rate on foreign companies has been brought down to 35%. Further, with a view to bolster the Indian start-up ecosystem, angel tax has been abolished. In light of the tremendous potential for cruise tourism in India the FM has proposed a simpler tax regime for foreign shipping companies.

On the policy front the FM has also announced an intent to introduce a simplified tax code, Tax Amnesty Scheme, concept of a Variable Capital Company structure for aircraft / ship leasing and pooled funds of Private Equity and increased efficiency in the IBC process which augurs well from an ease of business perspective.

Holistically viewed, the Budget ensured the continuity of competitive tax rates whilst responding to the demands of the middle-class and laying a solid foundation aimed at fostering sustainable growth and inclusive development.

As the Finance Minister rose to present the Union Budget 2024 of the new government, she did so with the advantage of a strong economy that provided the necessary springboard for the next generation reforms. The expectations from India Inc. were very high with continued structural reforms to realize India’s dream of being a developed nation and initiatives in infrastructure, domestic manufacturing, taxation, trade, land, labour, and the digital sphere.

First impressions from the Budget speech suggest that the Finance Minister has lived up to the expectations and has perhaps gone beyond with several proposals for investment, growth employment generation and tax reforms. The speech went beyond expectations by promising a comprehensive review of the income-tax law in the next 6 months, abolishing the regressive angel taxation and equalisation levy regimes, removing the distortion in buy-back taxation by reverting to taxation in the hands of recipients, announcing an expansion scope transfer pricing safe harbours, proposal to introduce another dispute settlement scheme etc. What was eagerly awaited however was a possible announcement on the direction of India’s tax policy for implementing the OECD’s global minimum taxation (GMT) rules. But with the promise of a comprehensive review of the income-tax law in due course, we may see a delayed or staggered implementation of the same in India. It must also be acknowledged that the OECD’s GMT rules has certain design related issues which need a wider and more comprehensive consultation before implementation. The system is particularly complicated and is conceived as a package of rules that countries simply add to their pre-existing tax systems, whose complexity, in most cases, was already preponderant. The level of difficulty is increased by the interaction with the rules with the pre-existing national and international systems, which already comprise a large number of anti-tax-avoidance rules. This level of complexity might be difficult to handle in some developing jurisdictions such as India, whose priority rightly should be to rationalise and improve the existing tax regime rather than add another layer of complexity. This was evident from FM’s speech where she emphasised on simplification of the tax regime. It should also be noted that the GMT does not curb tax competition but rather creates a new floor. Further, the GMT rules, as designed by the OECD, may raise fundamental questions around issues such as nexus and extra-territoriality, which need to be thoroughly examined so as to withstand any legal challenge. Indian headquartered international groups would now need to plan for their global obligations under the GMT rules in countries where they are enacted recognizing that India would further delay or stagger its implementations.

The first budget of the new government proposes significant tax and regulatory changes, while maintaining policy continuity in favour of economic growth..

Phase Manufacturing Programme (PMP): As a part of the ‘Make in India’ initiative, the PMPs support companies producing goods within India by encouraging domestic value-added production through the gradual increase of the basic customs duty (BCD) rates on parts, as production scales up in India. This budget expands the PMP to include the medical devices sector, reflecting the government’s policy continuity to boost domestic manufacturing, reduce import dependency, and encourage exports.

Recalibration of tariffs and correction of duty inversions: Custom duties for essential resources and export buoyancy sectors, including the critical minerals, textile, leather, and electronics goods (including mobile phones), have been recalibrated. This initiative aims to stimulate the growth of domestic manufacturing in sectors pivotal to India’s export economy, a

The FM also announced a six-monthly drive to address the issue of the inverted duty structure, a welcome development.Effective tackling of this issue would be crucial, however, given the liberalization of Free Trade Agreements (FTAs) and general exemptions, a vibrant stakeholder dialogue with trade and industry is essential for the success of this initiative.

Duty reduction on gold and other precious metals: The budget reduces the duty on high-value products significantly, with the effective duty on gold bars reduced to 6%. Historically, India has been conservative in reducing duties on these items due to their import dependency and potential impact on the CAD. This measure, though aimed at enhancing domestic value addition in gold and precious metal jewellery, also signals government’s confidence in financing CAD through inward remittances and investment flows, reflecting India’s growing global attractiveness.

GST related

There was an articulation of an intent for simplification of GST rate structure and expanding the base by possibly extending it to sectors which are currently outside the ambit. This presents an opportunity to the industry to make a case for inclusion of petroleum products (possibly starting with ATF and Natural Gas), electricity and real estate. The rate structure simplification is also significant, which would prompt the industry to assess the impact and present their views to the Government.

Many changes have been proposed to give effect to GST council decisions such as introduction of Section 11A to handle cases where incorrect GST application was due to prevailing practices.

Overall, the budget signals policy continuity, endorsing 'Make in India' and Ease of Doing Business.

Keeping in mind the vision of Viksit Bharat by 2047, the Finance Minister presented a finely-tuned Budget with a strong emphasis on employment, skilling, MSMEs and the middle class.

On the direct tax front, it is proposed to rationalize and simplify the capital gains tax regime by bifurcating assets into listed securities (eligible for a concessional tax rates) and other assets (subject to higher tax rates). Receipt from buy-back of shares is proposed to be taxed as dividend in the hands of the shareholder. A reduction is proposed in the rates of TDS vis-à-vis certain categories of transactions. To give a boost to the start-up community, the Government has proposed abolition of the controversial angel tax provision. Several amendments have been proposed to incentivize investment in IFSC.

With a view to reduce tax uncertainties and disputes, the Government has proposed to launch VSV 2.0 for settlement of pending litigation. Further, reassessment provisions are proposed to be rationalized and the outer time limit to reopen assessment is proposed to be reduced from 10 years to 5 years from end of the assessment year in certain cases.

On the international tax front, in a welcome move, the corporate tax rate applicable to foreign companies is proposed to be reduced from 40% to 35%. To ease tax burden on foreign e-commerce operators, Equalisation Levy of 2% is proposed to be abolished.

On the personal tax front, the common man will experience some relief. The Government has proposed to revise the tax rate structure for individuals opting for the new tax regime, resulting in effective tax savings of INR 17,500. The standard deduction is proposed to be enhanced from INR 50,000 to INR 75,000.

Lastly, in order to make the Income-tax Act, 1961 more concise, lucid and easy to understand, the Finance Minister has announced a comprehensive review of the Act, within six months.

Stakeholders were looking forward to the Budget providing greater clarity on India's implementation framework for BEPS 2.0. However, no announcements have been made by the Finance Minister on this front.

To sum up, India's first budget under a new coalition government has taken a balanced approach by outlining proposals that will not only address key issues on the tax front but also help the Government to achieve its vision of 'Viksit Bharat' in the 'Amrit Kaal'.

"The increase in standard deduction would, at the maximum, have the effect of reducing the tax liability by Rs 7,500 at the maximum slab rate. Employment Linked Scheme The schemes intended to generate more employment are all non tax incentives. Further, employment is organized sector alone is eligible for the benefits sought to be extended. Only those employees who are registered with the EPFO would be counted in for extending the benefit. This is a move towards bringing more organisations into organized sector. The benefit to “first time employees”, earning salary upto Rs 1 Lakh per month, is capped at Rs 15,000 per employee. The benefit would be provided as direct transfer to the employee. This will reduce the burden on the employers seeking to recruit fresh employees. The creation of additional employment in “manufacturing sector” would be incentivized in the form of reimbursement of part of EPFO contribution by the employer and employee. This scheme intends to operate for a longer period of 4 years. The larger scheme applicable to employers in all sectors is again linked to EPFO contribution by the employers for the additional employment created by them. EPFO contributions upto Rs 3000 per employee would be reimbursed for a period of 2 years from the date of creation of new employment. The rules relating to (a) determination of new employment generation, (b) determination of remuneration payable to them, (c) form and manner of application for the scheme, and (d) manner of receipt of the subsidy, are yet to be notified by the Government."

Positive & Growth oriented inclusive budget touching important aspects of employment, skilling, rural development, infrastructure, manufacturing, etc. Should help private sector to revive Capital expenditure. Large outlays to address important social infrastructure and regional imbalance to be addressed. Fiscal consolidation will be positive to attract investments. Employees are being encouraged to take benefits of EPFO. Several important tax changes made include following:

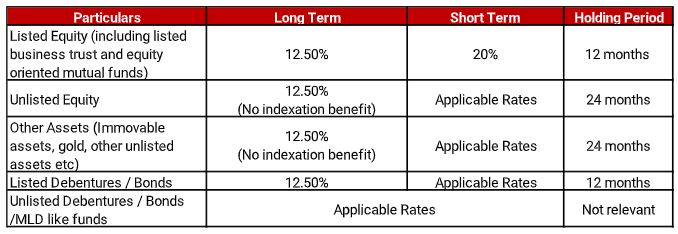

- Changes in capital gains tax rate increase covers equity shares REITS etc. 12.5% for all categories of assets and STCG 20%. Period of holding for listed (12 months) and 24 months for short term across assets.

- Seems that indexation benefits removed. It seems that 2001 FMV retained as eligible Cost for immovable property / other assets capital gains Computation.

- TCS to be deducted while computing TDS on salaries. No foreign tax credit adjustments covered.

- Extra standard deduction of Rs. 25000 if new Tax regime chosen.

- Rationalization of TDS rates (E.g. on rent, commission, etc. @ 2% Vs 5%).

- Foreign companies are to be subjected to 35% tax against 40% currently.

- Parity in TDS rates @ 0.1% under section 194-0 & section 194Q

- New Section 44BBC introduced to deal with taxation for non-residents engaged in domestic cruise activities. Tax to be charged on deemed profits of 20% subject to fulfilment of conditions.

- Section 56(2) (VIIb) dealing with taxation of any amount received by companies more than fair value being deleted from A.Y. 2025-26.

- Parity in tax rates on capital gains across residents and non-residents covered under section 115AD, 115AB, 115AC,115ACA and 115E with that prosed under section 112A/ 112B rates under section 111 A.

Several other amendments in direct tax to be evaluated as they seem to have far reaching repercussions.

The Finance Minister of India, Nirmala Sitharaman, in the first Budget Speech of the current government, outlined pivotal changes in taxation and fiscal policies. One of the most important announcements was the FM’s decision to undertake “a comprehensive review of the Income-tax Act, 1961” and to complete the process within 6 months.

The most awaited change was revision to the personal tax rates or the slabs. Under the new regime, individual taxpayers stand to benefit from revised tax slabs and an increased standard deduction to Rs. 75,000, by reducing the overall tax burden by Rs. 17,500. The FM has also enhanced the deduction towards pension scheme relating to employer’s contribution from 10% to 14%. Such increase is extended only in case the employee has opted for new scheme of taxation.

For corporate taxpayers, the maintenance of current tax rates signals continuity in policies aimed at bolstering India’s business climate and fostering investor confidence.

Effective from July 23, 2024, the Finance Bill introduces streamlined capital gains tax rules. Especially, long-term capital gains on various asset classes will now be taxed at a unified rate of 12.5%, simplifying the tax regime and ensuring parity between domestic and foreign investors. Adjustments to holding periods for assets like listed securities aim to stimulate investment activity while aligning with global best practices. Further, it is also pertinent to note that the FM has abolished the indexation benefit that was available on sale of long term capital assets.

In a move towards enhancing taxpayer experience, the FM has proposed measures to revise the time to reopen past assessment proceedings and rationalize TDS rates. This includes implementing timelines for refund adjustments and strengthening infrastructure to resolve pending appeals efficiently. The introduction of the Vivad Se Vishwas Scheme, 2024, is a major initiative by the government's commitment to reducing litigation and promoting tax certainty.

The Finance Bill also proposes critical reforms in indirect taxation. Rationalization of GST rates seek to rectify anomalies and ensure uniformity, while customs duty rationalization aims to boost domestic manufacturing under the ‘Make in India’ initiative.

The Finance Bill, 2024, represents a strategic blueprint for India’s economic trajectory under Modi 3.0 government, combining stability with progressive reforms. By addressing immediate fiscal challenges and laying the groundwork for sustainable growth, the budget highlights the government’s commitment to inclusive development and global competitiveness. The Budget sticks to the fiscal discipline which has come to be the hallmark of Modi’s Govt in all terms.

Hon’ble Finance Minister (FM) Nirmala Sitharaman presented the Union Budget 2024-25, which sets a new benchmark by showcasing India's political stability and continuity. It distinctly outlines priorities for a Viksit Bharat, with a strong emphasis on enhancing tax certainty through simplified and streamlined tax litigation processes. It focuses on enhancing foreign direct investments, generating employment, bolstering agriculture and thermal power sectors, empowering women, and advancing infrastructure development. The budget aims to uplift people with low incomes, women, youth, and farmers. Additionally, proposals were introduced to reform the Insolvency and Bankruptcy Code (IBC) and National Company Law Tribunal (NCLT) frameworks to expedite case resolutions.

Hon’ble FM accentuated the importance of enhancing the clarity and simplifying of The Income Tax Act, 1961, making it more accessible. Additionally, there is a strong focus on streamlining processes related to charities, TDS, litigation, appeals, reducing time for reassessment and reopening and expanding the tax base.

Echoing the Economic Survey's emphasis on good governance with continuing a historical trend, key direct tax proposals include:

- Abolishment of the angel tax provision [section 56(2) (viib)] which will bolster the startup ecosystem, enhance the investment climate, boost investor confidence, and stimulate economic growth.

- Introduction of the Direct Tax Vivad se Vishwas Scheme, 2024, to further simplify the tax regime.

- Withdrawal of the Equalization Levy indicates alignment with international initiatives such as the OECD's Pillar One.

- Overhaul of buyback tax following the abolition of Dividend Distribution Tax (DDT) and its treatment as deemed dividend has come as a surprise, affecting many restructuring plans of NRI investments.

Tax Administration and Tax Certainty:

A comprehensive review of the Income Tax Act, 1961, over the next six months, aims to simplify taxation and reduce litigation, reflecting the government's proactive approach to ease tax administration. This will reduce disputes and litigation, thereby providing tax certainty to taxpayers.

There's a reduction in tax litigation by limiting the reopening and reassessment period to up to six years, digitization of rectification and ITAT appeals within two years, with a restricted appeal scope at appellate levels. Further, to streamline guidelines for compounding and simplify charity and TDS procedures, there's a proposal to consolidate TDS rates for a few provisions of Chapter XVII.

Incentivizing Tax Provisions:

Relief measures for salaried employees, including adjustments in standard deductions and slab rates, benefit middle-income groups, resulting in a net INR 7,000 crore tax foregone by the Revenue Department.

Anti-avoidance Measures:

An overhaul of the buyback tax following the abolition of the Dividend Distribution Tax (DDT), treating it as a deemed dividend, has come as a surprise, affecting many restructuring plans of NRI investments. To mitigate disparities and curb unwanted tax planning, capital gains on financial assets have been increased to 20% (STCG) and 12.5% (LTCG), along with changes in the holding period for financial and non-financial assets and a reduction in long-term capital gains for non-financial assets from 20% to 12.5%, with an increased exemption limit for financial assets up to INR 1.25 lakh. The real estate economy is expected to boost as immovable property is taxable at 12.5% with long-term capital asset holding for two years. There will be no indexation benefit with consequent reduction of the base tax rate.

International Tax Proposals:

Expansion of safe harbour rules and streamlining transfer pricing assessments to reduce international tax disputes are major proposals that could be considered a move toward Pillar Two. Measures have been proposed to attract foreign investments, including reduced tax rate for foreign companies (40% to 35%) and simplified tax regimes for foreign shipping and mining entities.

Overall, these proposals aim to simplify tax compliance, promote economic growth, and enhance tax savings across sectors.

Other Proposals:

Other significant initiatives include encouraging states to lower stamp duties for properties purchased by women and amendments to the Benami Property Act to curb benami transactions. The budget also focuses on promoting IFSC - GIFT City, with proposals to remove thin capitalization, grant customs duty exemptions on specific medical, mineral, and solar products, and various initiatives in sectors like employment, tourism, innovation, research, digital infrastructure, and ease of doing business, aiming to propel India towards a technology-driven economy.

Overall, direct tax proposals bring certainty and stability to tax policies, which is crucial in creating a positive foreign and domestic investment climate in India. The clear trajectory of fiscal consolidation, with the fiscal deficit of 4.9% to GDP from 5.6% and 6.4% in FY 24 and FY 23, respectively, will significantly boost the economy to match international standards and set a growth path for India’s future.

“The first budget of Modi 3.0 government packs a lot of punches (some unexpected!). Overall, the budget announcements centred around employment avenues, continuing infrastructure spending, strengthening the social infrastructure, etc. It is good to note that the government has expressed its intention to reduce the fiscal deficit on a year by year basis. On the tax proposals, significant amendments have been proposed. One can observe multiple amendments on the customs aspect with a clear focus on making India a competitive manufacturing hub. On the direct tax aspects, the announcement of relooking once again at a new direct tax code is going to give sleepless nights in the coming months to tax professionals. Prior to the budget, it was expected that the Government would carry out Capital gains tax reforms and create a level playing field between residents / non-residents as well as different types of asset categories. While much has been done on this front, the removal of indexation would hurt the taxpayer, especially for investors in the real estate category. Also, the tax incentive to migrate abroad to become a non-resident has been reduced considerably. Some out of box changes such as deeming a buyback to be a taxable dividend is a surprise. Proposals for TDS and TCS rationalization is a welcome move. The codification of vivad se vishwas scheme 2024 in the finance bill to settle pending litigation would need a closer look. Removal of angel tax as well as equalization levy is “better late than never” move and brings cheer to the foreign investors and the start-up community. All in all, this is a budget with one of the longer finance bills and is likely to keep us engaged in deep conversations for the next few weeks.”

"The Union Budget 2024-2025, announced by the Government of India, marks a significant step toward realizing the vision of "Viksit Bharat" or “Developed India.” This forward-looking budget is designed to foster inclusive growth, enhance productivity, and ensure sustainable development across various sectors.

A key highlight of the Budget is its emphasis on job creation and skill development to harness the potential of India's youth. The proposed employment and skilling measures, including incentives for EPFO contributions and the upgrading of 1,000 Industrial Training Institutes, are expected to create millions of jobs and enhance workforce participation, particularly among women. This focus on human capital development is crucial for sustaining economic growth and improving living standards.

The Budget introduces several measures to streamline the tax regime, reduce compliance burdens, and promote entrepreneurship. Notably, the reduction in the corporate tax rate for foreign companies from 40% to 35%, the proposal to withdraw the 2% equalisation levy to provide relief to digital companies, and the abolition of the Angel Tax for all classes of investors are welcome steps. These reforms are expected to stimulate investment, particularly in startups and the digital economy, fostering innovation and competitiveness.

The Budget's proposals to tweak capital gains taxation are also noteworthy. While market reactions to these changes may be mixed initially, the strong fundamentals and foundation of India's capital markets should ensure that any negative sentiments are short-lived. The overall direction towards simplifying the tax regime and making it more business-friendly is commendable.

For the salaried class, the increase in the standard deduction and adjustments to the slab rates under the new tax regime are significant. These changes make the new tax regime more attractive, providing relief to taxpayers and potentially increasing disposable incomes. This move is likely to boost consumption and, in turn, spur economic growth.

Overall, the Union Budget 2024-2025 is a comprehensive document that lays the groundwork for a resilient and inclusive economy. By addressing immediate needs and setting the stage for long-term growth, the Budget reflects the government's commitment to making India a global economic powerhouse. The focus on job creation, tax simplification, and support for innovation and entrepreneurship will be key drivers in achieving this vision.

I view the Union Budget 2024-2025 as a forward-thinking and balanced approach to economic policy. It provides a clear roadmap for sustainable development, emphasizing the importance of human capital, innovation, and a business-friendly environment. This Budget positions India well to navigate global economic challenges and capitalize on emerging opportunities"

“The Finance Minister articulated the Government’s commitment towards a stable and simplified tax regime. The budget proposals outlined today emphasize on improving taxpayer services by leveraging technology, ensuring tax certainty and reducing litigation while broadening the tax base to garner revenue for developmental needs. Over the next six months, a thorough review of the Income-tax Act, 1961 is planned to simplify its structure and reduce complexity. The proposal to abolish angel tax will provide much needed respite to foreign and domestic investors alike.

Introduction of a dispute resolution scheme and higher monetary thresholds for filing appeal by tax department is a welcome initiative which will further help in streamlining tax litigation. The proposed phasing out of Equalisation Levy is in line with the global practices pursuant to the pillar 1 solution developed at the OECD G20 inclusive framework. The foreign investors will also cheer the reduction in corporate tax rate from 40 to 35 percent.

Capital gains tax regime is proposed to be simplified accompanied by higher tax impact on listed securities and increased STT on futures and options of securities. On the PIT front, there is definitely a nudge by the Government to opt for the new tax regime with increase in standard deduction, change in slab rates and enhanced deduction for employer contribution to NPS. Additionally, the budget outlines several long-term policy initiatives, including the preparation of a financial sector vision and strategy document, development of climate finance taxonomy, introduction of variable company structures for aircraft and ship leasing financing, and simplification of the FDI regime. Some of the proposals were focused for immediate solution to the taxpayers whilst the fine print of over 200 pages reflect that the changes proposed may be wide sweeping in their impact.”

The amendments to the CGST Act are as expected and reflects the implementation of recommendations of 53rd GST Council Meeting. Unfortunately while the Finance Minister spoke on increasing the number of benches of NCLT, NCLAT and DRT nothing much was said in the context of the GST Appellate Tribunal which is yet to be constituted.

While Section 16(5) is welcome and addresses the issue of time limit under Section 16(4), relief should also be provided for assessees who have not contested orders on 16(4) or reversed ITC during audit with interest.

In the customs front amendments to Section 65 is likely to restrict the scope and ambit of MOOWR which was getting popular.

The Indian government's budget aims to stimulate growth and employment by focusing on key sectors such as agriculture, manufacturing, services, and urban development. It emphasizes infrastructure development, energy security, and innovation, with initiatives like solar power programs and investment in space technology. The budget also proposes significant income tax reforms such as a comprehensive review of the Income Tax Act, 1961, with results expected within six months. Additional measures to ease the tax burden on individuals and businesses include merging the existing tax exemption regimes for charities, reducing the TDS rate for e-commerce operators to 0.1% from the erstwhile 1%, and allowing TCS credit against TDS deducted on salaries. To streamline tax administration and reduce litigation, reopening and reassessment procedures are being simplified, with standardized operating procedures (SOPs) for TDS defaults and rationalized compounding guidelines.

Capital gains taxation is being restructured, with differentiated rates for short-term and long-term gains on various financial and non-financial assets. The "Vivaad se Vishwas Scheme 2024" aims to expedite the resolution of tax disputes, and the abolition of angel tax is expected to provide a significant boost to the Indian startup ecosystem. Under India's Black Money Law, a penalty of INR 10 lakhs was previously levied for failing to report foreign assets exceeding INR 5 lakhs in bank accounts on income tax returns. This particularly affected Indian employees of multinational companies receiving ESOPs and individuals investing in foreign shares who unintentionally omitted these assets in their tax filings.

The Budget has raised the exemption limit to INR 20 lakhs for all types of undisclosed foreign assets. This amendment significantly benefits those who acquired foreign assets up to INR 20 lakhs from taxed income but failed to report them, as they are no longer liable for penalties under sections 42 and 43. However, individuals who acquired foreign assets from untaxed income will still face penalties such as a 30% tax and a 90% penalty.

The government has also introduced significant updates by incorporating changes from the latest GST Council meeting. Key updates include the exclusion of Extra Neutral Alcohol (ENA) used in alcoholic beverages from GST. Deadlines for claiming input tax credits from previous years have been extended, and pre-deposit amounts for filing appeals have been reduced. Businesses can avoid interest and penalties on past tax dues by settling their liabilities by a specified date. Recent updates clarify the treatment of certain services under GST and simplify invoicing and return filing processes, including mandatory GST TDS returns even without transactions. In response to the non-constitution of the GST Appellate Tribunal (GSTAT), the time limit for filing appeals has been adjusted to prevent cases from becoming time-barred, and provisions have been made for handling anti-profiteering cases with a sunset clause.

Budget this time should be looked upon not necessarily from the tax amendments but more from strategic thrust which it proposes to make on the side of employment and filling up the skill gap. It is heartening to see that the Givernment has taken the issue of employment on a very comprehensive basis. This includes creating demand for new employment (incentivising the new employees) and also ensuring adequate supplies (skills and internship programmes). This would go a long way in the growth strategy for the country and productive utilisation of India’s youth.

In the coming year 2024-25, India’s total receipts would be close to 32 lac Crores comprising of primarily 10 lac Crores of GST (only IGST) and 21 lac Crores of Income Tax. Fiscal deficit is likely to go below 5% of GDP and more importantly likely to reduce in absolute terms as compared to the revised estimates of 2023-24.

It is also important to note that the capital expenditure is likely to go to 11.11 lac Crores from last year’s 9.5 lac Crores. This is impressive. Just to understand the scale of increase the Capex for 2022-23 was 7.40 lac crore. There is an increase of 50% in just three years.

Coming to the tax proposals the most significant change is in the capital gains tax. While removing the indexation benefits they have reduced the LTCG tax rates from 20% (effective tax rate of 24.11%) to 12.5% (effective 15%). Further tax rates on LTCG have been made uniform across the asset classes. Even holding period for an asset to become long term has been made uniform to 24 months except listed shares which co to use to be 12 months.

Further once again in search cases the block assessment scheme has been introduced similar to earlier scheme with some modifications. There is also a major change made for time limit in reopening assessment and introduction of Vivad se Vishwas Scheme. On the whole the budget has balanced provisions.

The budget is well-rounded as it addresses both immediate challenges and is future focussed. The Government has demonstrated fiscal prudence while prioritizing employment, skilling, MSMEs, and the middle class in its budget announcement. On the tax proposals, efforts to improve ease of doing business in India are evident through measures such as reducing foreign company tax rates and abolishing the angel tax. A comprehensive review of the Income Tax Act, 1961 is expected to offer opportunities for further simplification and rationalization. Additionally, the Vivad se Vishwas scheme 2.0 aims to enhance dispute prevention and resolution. While the increase in long-term capital gains tax may disappoint investors, the positive side includes an expanded limit for capital gains exemption. Overall, the budget aims to set the path for India’s future growth and development.”

“Budget this year was expected to be a policy document laying out long term vision of sustained high economic growth, and it’s fair to say that the government has done a wonderful job of articulating this vision, linking to 9 macro-economic priorities. Focus on inclusive growth is a predominant theme of this Budget exercise, as there is a policy push for social and women development, agricultural growth, accelerating growth of manufacturing and services exports. Energy transition and Infrastructure growth has got the due attention, and one should expect more details to come out as the government rolls out Energy transition Pathway document.”

Cut in tax rate for foreign companies from 40 to 35% and the abolition of the 2% equalization levy was a surprise. Logically these would be replaced with alternative levies in the run up to implementing Pillar 1 and 2 obligations. Unlike individual tax refunds which appear to be aplenty the same situation was not applicable for corporates. The benefits of order giving effect digitalization would hopefully go a long way in unlocking refunds.

Financial services sector has received lot of attention in the Budget this year and rightly so. The government intends to bring out a financial sector vision and strategy document to set the agenda for the next five years and guide the work of the government, regulators, financial institutions and market participants. This would hopefully take holistic view of what is needed to strengthen the financial ecosystem that keeps in mind India’s long terms inspirations and helps mobilise capital in the right pockets.

Globally Variable Capital Companies are widely used for different purposes especially in the popular jurisdiction where funds are domiciled. The financial service regulator in GIFT city IFSCA has been closely working on introducing VCC structure for funds in IFSC. The Government intends to introduce this structure for PE investments and leasing of aircraft and ships. Currently most of the funds are set up as trusts and leasing business is carried out as companies in line with RBI’s current regime that governs non-banking financial companies. The VCC structure will combine the advantages of the company with the operational ease of introducing fresh capital from new investors and redemption to existing investors.

Capital gains rates which have direct impact on the stock markets and thereby moving domestic saving into capital markets, would undergo a major change not just in terms of increasing tax rates from 10% to 12.5% and 15% to 20% on listed equity and equity mutual funds but on the whole aims to simplify the regime by reducing rates and holding period into fewer categories. This will ease compliance and is likely to reduce a few pages from bulky tax return form. Increase in STT rates on derivatives is in line with the concerns expressed in the Economic survey and by the markets regulator regarding excessive speculative activity.

Reduction of corporate income tax on foreign companies from 40 to 35% will provide relief largely to foreign companies doing in the business in India in the form of branches (eg. foreign banks), project offices and other forms of what creates a taxable presence in the from of a ‘Permanent Establishment’ under the tax treaties.

Budget 2024 sticks to rhetoric of tight rope walking as seen in the past years to ensure we adhere to the fiscal discipline targets. The allocation to railways, science and technology or AI /deep tech don't appear to have a steep raise, growth in tax collection have been assumed at 10 percent perhaps factoring a slowdown in GDP growth to 6.5 percent while assuming favourable conditions exist for fertilizer and fuel subsidies.

Corporate India which has had the benefit of lower tax rate of 25 percent will have to wait for details to emerge on the simplification measures which will arise on tax compliance and on the amnesty scheme to free up litigation. States in India which clamoured for abolition of undivisble Cess pool will have to wait as cess continue to exist and GST litigation likely to be an offshoot.

The budget proposal continue with the theme of year on year anti abuse provisions being added which have proposed interalia buy back being taxed as dividends, property income being taxable only as house property income, provisions being made to deny settlement made by corporates as part of business with regulators, being disallowed as a business expense and also indexation benefits being discontinued for long term capital gains.

Personal taxpayers have some limited room to cheer with token adjustments to slabs and standard deduction being revised.

In summary with the theme on boosting first time employment, skill development and aiding growth of States and regions which have suffered from natural calamities and lack of industry to provide gainful employment, a start has been made for reforms.

If the schemes which propose reduction in tax litigation and tax compliance, become a reality corporate India will have room to cheer. Getting all states on board and ensuring equitable development and state sponsored schemes m will be crucial to get us moving towards Viksit Bharat. Also, the countdown to GST rate rationalization is one big theme waiting to unfold and relevant as reforms continue!

The Union Budget 2024, presented by Honourable Finance Minister Mrs. Nirmala Sitharaman, was an important moment after the formation of the new government, and it emphasized a strong commitment to tax simplification, enhanced taxpayer services, and efforts towards reducing litigation. This budget re-emphasized the Government’s objective of fostering a business-friendly ecosystem and projecting optimism for the future.

One of the bold steps in this direction is the announcement to comprehensively review the Income-tax Act, 1961, within 6 months, with the aim to streamline and simplify it. However, it will be crucial to ensure this does not inadvertently lead to increased interpretation issues and more litigation!

Another standout announcement is the reintroduction of the previously tried and tested, Vivad se Vishwas scheme, aiming to settle pending tax disputes amicably, showcasing the government's proactive stance on minimizing litigation. Additionally, measures such as rationalizing reassessment timelines, increasing monetary thresholds for revenue appeals, and enhancing safe harbor rules for transfer pricing are aimed at further reducing the tax litigation and provide tax certainty.

Further interesting reforms include rationalizing appeal filing deadlines, increasingly empowering the Transfer Pricing Officers to identify specified domestic transactions and announcement to streamline the transfer pricing assessment procedures.

The streamlining of capital gains tax, featuring simplified holding periods and a unified 12.5% rate for long-term gains by abolishing indexation, alongside enhanced parity between resident and non-resident taxpayers, appears to have been well-received by the stock markets, with no immediate major corrections observed in the indices. However, the increase in the short-term capital gains rate on STT-paid securities from 15% to 20% has come as a surprising development.

Notably, much anticipated announcements on Pillar 2 were absent from the Budget speech, which may await future developments.

In essence, while Union Budget 2024 appears strongly focused on tax reforms aimed at reducing litigation and fostering stability, a detailed review of the Finance Bill will provide deeper insights. Initial reaction to the budget seems that these reforms underscore the government's proactive approach in creating a predictable tax environment, crucial for sustained economic growth and attracting foreign investments.

“Budget 2024 proposes multiple amendments including those recommended by GST Council in its 53rd Meeting. While specific proposals warrant an immediate evaluation, the FM’s mention of focus on rationalizing the rate structure and inclusion of excluded sectors remains an area to watch out for. The highlight of the Budget was the proposal to eliminate the distinction between fraud and non-fraud cases for limitation period dovetailed with input tax credit being allowed for all cases post 31st march, 2024, irrespective of the nature of adjudication. While this, penalty distinctions for these categories are proposed to be continued. Another highlight of the Budget was announcement of the contours of amnesty scheme for Section 73 demands linked to FY 17-18 to FY 19-20. While the coverage prescribed is large with disputes at different judicial levels being covered and those matters too which while initiated under Section 74 are upheld as Section 73 matters, restricting the scheme to cases where full tax under the notice/ order is paid may restrict the benefits envisaged under the Scheme with benefits not being available for those notices with multiple issues and cherry picking of issues was being considered. Another key proposal is enabling clause for granting powers to the Government for regularizing specified tax dues linked to prevailing general practice. These would go a long way in aiding tax certainty in India and curtailing unwarranted litigations for businesses. Other key proposals in the Budget include insertion of enabling provision for prescribing sunset for anti-profiteering provisions, rationalized provisions for determining time of supply for reverse charge supplies, regularizing issues linked to transition of ISD credits and distribution under the GST era, etc. Rationalization of customs duty rates are expected to further foster ‘Make in India’ objective and deepen value addition in India. Industry must continue to monitor the proposed comprehensive review of rate structures to analyse impacts on their businesses. Also, proposals for enabling acceptance of different proofs of origin for duty benefits under trade agreements would help contain on-ground procedural challenges. Separately, businesses would keenly watch out for prescriptions on sectors not covered for benefits under manufacturing in bonded warehouse. All-in-all, announcements in this meeting were a great start of innings for the new Government and industry would look forward to this continued focus on trade facilitation and ease of doing business.”

“The introduction of formula based indexed cost for shares transferred under Offer For Sale under an Initial Public Offering will lead to higher taxation for the promoters”

“The abolition of Angel Tax is a welcome move and this will go a long way in attracting foreign investments into India and helping domestic companies to avail different sources of funds for their growth.”

“The buyback taxation change can lead to litigation as buyback under Companies Act can be done in more than one way whereas the provision only covers a particular way of buyback to be considered as dividend income for the recipient. This was the case even when the buyback provisions were introduced and the same lead to litigation.”

Budget 2024 Reshapes Indirect taxes for Growth and Compliances

Today, Finance Minister Smt. Nirmala Sitharaman presented the highly anticipated Union Budget 2024 marking the first fiscal blueprint of the current government. This Budget, set against the backdrop of global economic uncertainties and India's aspirations for accelerated growth, outlines the government's financial priorities and economic vision for the coming fiscal year. From an indirect tax perspective, with a focus on simplification of compliances, reduction of litigation, promoting local manufacturing and local value addition, the following important updates were announced:

The FM has announced reduction in customs duty on various items with an aim to reduce the input costs, deepen the value addition, promote export competitiveness, correct the inverted duty structure, and boost domestic manufacturing (with effect from 24 July 2024). Accordingly, import duty on 25 critical minerals, inputs and capital goods required by the aquafarming and marine sector, textile and leather sector and precious metals has been reduced. With a three-fold increase in domestic production and almost 100-fold jump in export of mobile phones over the last 6 years, the FM has now proposed, keeping the interests of consumers in mind, a reduction in basic customs duty to 15% on import of mobile phones, mobile phone chargers and printed circuit board assemblies (PCBA). Similarly, the prevailing exemption for various commodities such as lithium-ion cell used in the manufacture of battery and battery packs for cellular mobiles and EVs under Notification No. 50/2017-Cus now stands extended upto 31 March 2026, with certain commodities like drugs and materials, life saving medical equipment, capital goods, raw materials and spares for repairs of ocean-going vessels stand extended till 31 March 2029.

Many legislative amendments relating to the recommendations made in the recently concluded 53rd GST Council meeting too have been introduced through the Finance Bill. A gist of the important updates includes exemption of Extra Neutral Alcohol used in the manufacture of alcoholic beverages from the GST regime. The government is also empowered to now regularize non-levy or short levy of GST due to prevalent trade practices.

Input tax credit availment time limits have been increased retrospectively from 1 July 2017, for specific financial years and situations. This includes provisions for the initial years of GST implementation (2017-18 to 2020-21, time limit increased to 30 November 2021) and cases where returns have been filed after revocation of registration cancellation.

A new Section 74A establishes common time limits for issuing demand notices and orders from FY 2024-25 onwards, covering cases whether or not involving fraud, suppression of facts, or wilful misstatement. This would mean that time limit for issuance of notices to taxpayers not being accused of any fraud etc. has been increased by 9 months (to 42 months instead of 33 months) but time limit for someone suspected of perpetrating a fraud / suppression / wilful misstatement has been reduced by 12 months (from 54 to 42).

The maximum amount of pre-deposit payable for filing appeals at various levels is being reduced along with the percentage of pre-deposit payable as well. This will result in reduced blockage of working capital. Additionally, a conditional waiver of interest and penalties has been introduced for Section 73 related demands (except erroneous refunds) for the period FY 2017-18 to 2019-20, if the tax amount is paid before a date to be announced.

Other notable amendments include introduction of provisions barring a refund (unutilised ITC or IGST) on goods subject to export duty, provisions for authorized representatives to appear on behalf of summoned persons, empowering the government to specify cases to be heard only by the Principal Bench of the Appellate Tribunal, and restricting penal provisions for certain e-commerce operators.

By introducing these reforms, the government seeks to create a robust and user-friendly GST framework that supports India's economic growth while ensuring fair and efficient tax collection.

“At a macro level, the budget aims to foster economic growth, enhance productivity, and create an investment ready and business-friendly environment with major initiatives to boost manufacturing sector such as industrial parks in 100 cities, major upgrade in the agriculture sector, tourism development, simplified FDI regulations, etc. Customs duty exemptions on critical minerals like lithium, copper, cobalt etc. will enhance the competitiveness of domestic manufacturing, promoting deeper backward integration. Reduction of customs duty on specific inputs for manufacture of leather and textile garments, coupled with ‘Employment Linked Incentive’ schemes, should encourage further investments in this labour intensive sectors. The intention to simplify Income-tax Act is not new but time will tell on how this would be rolled out and reduce the current complexity. However, steps taken towards ease of doing business such as abolition of angel tax, withdrawal of equalization levy, proposed amnesty scheme under VSV and reduced corporate tax rate for foreign companies are welcome.”

The budget with the Finance Bill 2024 is a mixed bag as far as direct tax provisions go.

Increase in tax free income for individuals, increase in tax exempt capital gains, removal of equalisation levy, removal of angel tax, reduction in tax rate for foreign companies, reduction in holding period of several assets from 36 months to 24 months for treating them long term, lower long term capital gains tax across all assets are some of the beneficial provisions in relation while rationalising capital gains tax. However, removal of cost indexation is a huge blow since taxpayer is penalised for increase in price merely due to decrease in value of rupee! Reduction of TDS on e-commerce from 1% to 0.1 % is significant and should give a big boost to digitalisation. Offsetting of TCS against TDS on salary should be a good relief to the cash flow if salaried class. Increase in threshold of disputed tax for the Revenue to go in appeal should have desired impact on reduction of litigation, so would the second Vivad se Vishwas scheme proposed

However, increase in rates of capital gains tax from 10% to 12.5% on long term capital gains and from 15% to 20% on short term capital gains, without any grandfathering provision is a big blow. This could have significant impact on flow of foreign capital especially where the credit for Indian capital gains tax is not available. It seems like in the effort to get revenue from big gains made by legacy property holders, a large number of investors are getting penalised. Equally, while change in taxation of Buy-Back of shares has a positive side of removing tax arbitrage possibility and consequent litigation, the proverbial baby being thrown out with bath water has happened by treating it as dividend, which should have been capital gains. Even the cost of acquisition of those shares will be available as deduction only against future gains. What if there is no gain from such shares in future? Requiring the shareholder to pay tax on gross consideration at marginal rate is clearly penal.

The Budget provides a definite thrust to promote Make in India by addressing the issue of inverted duty structure in Customs laws targeting specific sectors like nuclear, solar energy, leather and textile industries, marine exports etc. It has also announced a comprehensive revamp of customs duty structure to be carried out in next six months to rectify the inverted duty structure and reduce disputes. Another welcome measure is acceptance of self-certificate, as provided by the new trade agreements, as sufficient proof of certificate of origin. This should reduce the ambiguity and subjectivity in assessment of imports under Free Trade agreements.

The changes in GST law have been carried out largely to implement the changes proposed by the 53rd GST Council meeting. Thus, provisions allowing input tax credit to be taken till 30th November 2021, classifying no supply of transactions between co-insurer and lead insurer, exemption from compensation cess on supplies to SEZ developers, units etc have been duly incorporated.

Aligning the period for raising tax demand to a uniform time limit of 42 months and permitting the input tax credit of taxes paid under such demand irrespective of allegations of fraudulent intention may discourage the indiscriminate use of issuing tax notices alleging malafide intention.

Permitting authorized representative like employees, legal counsel or chartered accountants to appear in response to summons issued should provide relief from the practice of summoning senior officials of the company.

Hon’ble Finance Minister presented the much-awaited Union Budget today with a strong note of highlighting the priorities as employment generation, human resource development, sustaining the same focus on infrastructure development, productivity and resilience in agriculture etc.

On the direct taxes front, the finance bill is a mixed bag with some expected and unexpected proposals.

The angel tax provisions which were amended in the earlier budget drew lot of reaction from the nonresident investor community. In response it is proposed to drop the angel tax provisions as to its applicability from the FY 2024-25. This is a great news to the start-up industry. In line with the best practices foreign company tax rates are reduced from 40 per cent to 35 per cent. Rationalization of TDS rates is a welcome proposition. Eligible remuneration limits to working partners in a firm have been increased in response to various representations.

Search assessments procedure has always been under review from time to time. It is now proposed to reintroduce block assessment provisions with effect from 1st September 2024 and the block period shall consist of previous years relavant to 6 assessment years preceding the previous year in which the search was initiated under sec. 132 along with the broken period starting from initiation of search proceedings and closure of search proceedings in the year of search. The concept of undisclosed income along with the plethora of decided case law of the past would be relavant in the advent of this proposal.

Comprehensive Review of the Income Tax Act,1961 has been announced with an objective to make the Act concise, lucid, easy to read and understand. Thereby reduce disputes and litigation and in turn provide tax certainty to the taxpayers. This agenda is proposed to be completed in 6 months period. In light of this major policy announcement, the much-discussed Global Minimum tax under Pillar 2 GloBE rules has been put on hold for the present.

Rationalization of capital gains provisions is met with a mixed reaction. There is a focused effort to reduce litigation and in line with the same ‘Vivad se Vishwas scheme,2024’ has been proposed.

On the personal taxes front an effective tax savings of INR 17,500 has been proposed on account of revising the tax slabs under the new regime. Standard deduction is proposed to be increased to Rs. 75,000 from the present Rs. 50,000.

Equalisation levy 2.0 at the rate of 2 per cent on non-resident e-commerce operators has been proposed to be dispensed with effect from 1st August 2024, in line with the commitment as part of the Inclusive framework of the OECD-G20 BEPS initiative 2.0.

It is evident that the present budget is very balanced and forward looking one which stands out as a signpost of “Viksit Bharat”.

Union Budget 2024 - Key Highlights

The Finance minister marked a historic achievement on 23rd July 2024 by presenting her seventh consecutive Union Budget. The Union Budget 2024 provides a good impetus to infrastructure with an outlay of Rs. 11,11,111 crore which is 3.4% of GDP. FM also mentioned that the fiscal deficit for FY 2024 would be 4.9% of GDP and committed to reduce it to 4.5% of GDP in next year a very welcome move.

To reduce the compliance burden, promote entrepreneurship spirit and provide tax relief to citizens, following key direct tax proposals were made by Finance Minister:

(A) Rationalisation of capital gains -

a. Short-term capital gains on financial assets to attract 20% tax rate

b. Long term gains on all financial and non-financial assets to attract a tax rate of 12.5%

c. Increase in limit of exemption of capital gains on financial assets to Rs. 1,25,000 per year

d. Holding period for short term and long term has been rationalised to 12 months and 24 months respectively

e. Indexation benefit for long term capital assets has been removed and long term capital gains would taxed at 12.5% instead of 20%

(B) Employment and Investment -

a. Abolishment of Angel tax for all class of investors

b. Simpler tax regime to operate domestic cruise by foreign liners

c. Provide safe harbour rates for foreign mining companies (selling raw diamonds)

d. Corporate tax rate on foreign companies reduced from 40% to 35%

e. Incentives for operations in IFSC:

i. Specified funds under to include retail funds and Exchange Traded Funds in IFSC.

ii. Specified income of Core Settlement Guarantee Funds set up by recognised clearing corporations in IFSC, is proposed to be exempted

(C) Simplifying New Tax Regime -

a. Standard deduction for salaried employees increased from Rs. 50,000 to Rs. 75,000

b. Change in income tax rates - Income upto Rs. 3Lakhs will have Nil tax and income above 3Lakhs and up to 7Lakhs will attract 5% tax rate. This is a great move as the taxpayers would have an expected saving of Rs. 17,500 under revised tax slab rates.

c. Increase in amount allowed as deduction to non-government employers and their employees for employer contribution to a Pension Scheme referred in section 80CCD from 10% to 14%

d. Withdrawal of equalisation levy on e commerce transactions.

(D) Simplification of Taxes -

a. FM to come out with a comprehensive review the Income Tax Act, 1961 which is a welcome move but appears a tall order given 6 month's time frame.

b. Simplification of charities and TDS provisions

c. Amendments proposed for reduction in litigation and appeals by revising the monetary thresholds for filing an appeal and time limits for re-opening of assessments

d. Re-introduction of Vivad se Vishwas Scheme 2024

e. Withdrawal of equivalisation levy for ecommerce operators

Overall, it is a balanced budget without big reforms, but it has managed to address some expectations of middle class and its NDA partners. To conclude, the Union Budget 2024, while retaining the fiscal prudence, could be considered as a growth-oriented budget.

Finance Minister Nirmala Sitharaman presented her seventh consecutive budget today in Parliament. The Union Budget 2024-25 endeavors to reinforce the government's ambitious vision of the Viksit Bharat by 2047 by creating a robust and all-encompassing economy. Accordingly, the focus of this budget seems to be simplifying the income tax structure, reduce tax disputes & litigation, provide certainty to the taxpayers and improve the ease of doing business in India.

Pursuing the agenda of simplification & ease of doing business, the Finance Minister has announced a comprehensive review of the Income Tax Act,1961 within next 6 months. As an immediate measure, the budget has proposed simplification of the tax structure for charities, rationalizing tax rates for TDS & Capital Gains, simplifying provisions related to reassessment and decriminalization of certain offences for TDS. In another measure to reduce pending litigation & disputes, the Finance Minister has proposed to increase the monetary limits for filing of appeals and announced the Vivad se Vishwas Scheme 2024 for matters already pending in appeal. This reflects government commitment to provide tax certainty & make the overall environment conducive for businesses.

The initiative taken with regards to reduction in the corporate tax rate for the foreign companies, expanding tax benefits to funds & entities in IFSC, abolition of equalization levy for e-commerce, abolition of angel tax etc. are also aimed at providing much needed boost to the Indian economy by attracting more investments in India.

“It’s a progressive budget. It has laid the foundation of Viksit Bharat. The Union Budget bears footprint of a strong government with an extenuating effect of a coalition government. In terms of the tax proposals, the ethos being taking corrective and rationalisation path. There are some intrepid steps, like increase in capital gains tax rates particularly for listed securities. This could not have been done in fag end of the ruling term. The removal of indexation benefit for real estate sector comes with the sweet bitter pill for the middle class. Though, there is a removal of indexation benefit but at the same time lowering of tax rate, with added sweetener in form of slight relaxation of personal tax rate slab. There is also a change in tax methodology of buy back of shares. This appears to be a more burdensome as it may increase the tax outflow. Overall, this year budgetary tax proposals are towards the rationalisation and not for appeasing the common man.”

In one of the major announcements, the Hon’ble FM proposed to abolish the Angel Tax. This is a huge relief for Indian companies, specifically the start-ups. A delight for investors and PE/VC funds supporting Indian companies.

First budget of Modi Government 3.0 has proposed certain significant amendments aiming at reducing tax litigation/disputes and providing tax certainty. Amongst such proposals, one of the key proposals is to introduce the Direct Tax Vivad Se Vishwas Scheme, 2024. Though the scope and ambit of the scheme will be notified by the central government in due course, however it is possible that the government will introduce such amnesty scheme similar to the one launched in the year 2020 which had resulted in settlement of sizable backlog of pending appeals.

Similarly, the government has proposed to enhance the monetary limits in respect of the Revenue’s appeals filed before the higher judicial authorities/courts. This again will lead to deep clogging of the unwarranted litigation and would result in saving of time, cost and effort for both tax payers and tax administration.

Another game changing proposal is to reduce the limitation period of re-assessment from the existing period of 10 years to 5 years in respect of the cases where the income escaping assessment is more than 50 Lakhs. This way the hanging sword of uncertainty will not dangle over the tax payers head for an unreasonable period of time.

All these proposals we believe, will provide complete tax certainty to the tax payers and are steps in the right direction, considering the enhanced usage of technologies by the Income Tax Department in the recent years.

In the budget speech, there was a mention of a proposal to simplify the Income Tax Act in the next 6 months. This has been a long-awaited request from taxpayers over the past few years. In line with the simplification announcements, certain changes for simplification of the tax deduction regime have been announced.

One of the few key amendments on the income tax front has been an increase in the capital gains tax rates with a major change being the removal of indexation benefit provided u/s 48 proviso. This will be very harsh especially in cases of immovable property which has been held for a long period.

On the tax rates there have been revisions in the tax slabs under the new tax regime with the standard deduction increased to INR 75000 from INR 50000 for salaried employees.

On the transfer pricing front, the budget speech mentioned the expansion of the safe harbour rules, and also the streamlining of the transfer pricing procedures. We must wait for the revised safe harbour rules to review the details.

In an endeavour to reduce tax litigation, the Vivaad se Vishwas scheme 2024 has been announced to resolve pending tax disputes and also the limits for filing appeals have been increased.

Further major key announcements include angel tax abolishment for startups and the 2% equalization levy abolishment. In addition, there is also a boost for the startup sector with the mudra loan scheme.

In summary, the Indian budget 2024 emphasized simplification and growth, which is the need of the hour."

The Government has announced some big bold direct tax changes in the Union Budget, 2024. This includes abolition of angel tax and the 2% Equalization Levy. The rationalization of capital gains tax regime is very welcome – however, there are tradeoffs since there is an increase in the long term capital gains tax rate for non-residents and residents (in case of investments in listed securities). Reduction in tax rates applicable to foreign companies from 40% to 35% will bridge the CIT rate gap between Indian companies and foreign companies. The Government has brought about parity in taxation between dividends and share backs (however the benefit of cost of acquisition has been deferred, which will not be available as a capital loss to set-off future capital gains). Another big welcome change is reduction in the timelines for reassessment to 5 assessment years (10 assessment years added significant tax uncertainty).More nuanced tax changes relate to removal of tax exemption around corporate gifts (which was debated up until bow). All in all the Government has kept its ear on the ground and has taken industry feedback on board.

Changes to Benami Law:

- There is a proposal to provide immunity from prosecution to Benamidars and certain other persons (abettors) that come forward and provide evidence pertaining to a benami transaction. Such an ‘immunity’ is provided subject to such Benamidars complying with ‘conditions’ contained in the ‘tender of immunity’.

- While this is a crucial development that can impact ongoing Benami proceedings, uncertainty persists regarding what kind of ‘conditions’ that can be included within the tender of immunity. It remains to be seen if suitable guidelines are introduced giving clarity on what such conditions could be. Furthermore, it remains unclear whether other civil proceedings as well as penalty proceedings under the Benami Act can continue against such Benamidars when immunity is provided solely from ‘prosecution’.

- The proposed amendments enhance the administration’s investigative capabilities in collection of evidence. This coupled with the Government’s reaffirmed commitment towards digitalizing asset records (including real estate as mentioned in the budget speech) gives the administration a shot in the arm for ongoing as well as future proceedings.

Changes to Black Money Law:

- Under the unamended Black Money Act, failure to disclose foreign assets (except for bank account balances upto INR 5 Lakhs) by taxpayers in their return of income could lead to a hefty penalty of up-to INR 10 lakhs. Such stringent provisions have in the past caused hardship to small taxpayers, who failed to disclose minor assets located abroad. In particular, Indian residents holding ESOPs in foreign companies, foreign return students, etc have faced hardship for failure to declare minor foreign assets located abroad.

- With a view to decrease the hardship on small taxpayers, the Government has limited the applicability of penalty provisions on non-disclosure of foreign assets (excluding immovable property) only to scenarios where the aggregate value of such foreign assets exceeds INR 20 lakhs. This is a welcome move and will save small taxpayers from the hassles of penalties and litigation and around Black Money Law and lead to greater efficiency in allocation of administrative resources.

Empowering India through focus on MSME [MSMEs, Skilling, Middle class, and Employment]

The FM has kept her promise of announcing a substantive budget to start the Modi 3.0 era. The Budget continues the path of higher capital outlays, reforms and aptly addresses the four focus pillars - Poor, Women, Youth and Farmers. There was a specific focus on MSME: -

- The M is incentivized through a package covering financing in the form of credit facilities, regulatory changes, and technology support to help them grow and compete globally.

- The S and E is covered through announcement of a five-schemes package and initiatives to facilitate employment, skilling and other opportunities for youth of the country including empowering the women, over a five-year period.

- The Middle-class benefits from changes to personal tax, EPFO transfers and revamping the pension scheme.

It also proposes various tax rationalizations and simplification measures across direct and indirect taxes. While the FM gave a pass to extending the 15% tax rate for manufacturing, an overhaul of the capital gains tax regime and FDI changes will lead to mobilization of additional tax revenues. The introduction of a new Vivad Se Vishwas scheme is welcome to mitigate tax litigations. While the proposal to abolish angel tax is welcomed, the start- up sector is left wanting with no other major support. Given India has been a front-runner on the BEPS project, the move to withdraw equalization levy gives limited guidance on India’s alignment with Pillar 2 project.

All this, with yet another attempt to review and overhaul the Direct Taxes laws in the next 6 months –the FM will have her hands full. Overall, while a long-term planning for the 5-year regime has been outlaid by addressing multiple aspects, the key lies in implementation and certainty of benefit flowing to the involved stakeholders to achieve the desired goals.

A stable budget on indirect taxes

If stability and continuity is a desired virtue in administration of taxes, the provisions of the Finance Bill (No 2) announced in the budget meet the expectations.

The customs duty rates on certain items have been carefully recalibrated in line with the needs of the economy ostensibly to boost domestic manufacture and exemptions thoroughly reviewed. Certain trade facilitation measures such as increasing the time-period of duty-free re-import of goods (other than those under export promotion schemes) exported under warranty are proposed. The finance minister in her speech also committed to undertake a comprehensive review of the rate structure over the next six months to rationalise and simplify it for ease of trade, removal of duty inversion and reduction of disputes.

On GST front the provisions related to demand and recovery have been merged into a new Section 74A in the CGST Act to provide a common time limit for issuance of demand notices and orders in respect of demands for FY 2024-25 onwards. Other legislative changes are proposed to implement the recommendations in the recently concluded 53rd meeting of the GST Council. One proposed change, an offshoot of the recommendations, is to allow input tax credit on invoices or debit notes during the period of cancellation of registration, which is later revoked, by filing return within prescribed period. The taxpayers should also welcome removal of the restriction on input tax credit where tax was paid as a result of sustained allegation of fraud, wilful mis-statement or suppression or was paid during detention and seizure of goods in transit.

The Hon’ble Finance Minister (FM) tabled the Finance Bill No. 2 for the year 2024 today. In her budget speech the FM stated that intent of the Government is to simplify taxes, improve taxpayer services, reduce litigation and provide tax certainty. Is the fine print in line with the stated objective or there is a ‘devil hidden the fine print’?

On simplification, the proposed abolition of ‘Angel Tax’ and reduction of tax on foreign companies to 35% is an excellent step and so is the intent to merge the two tax regimes for charitable trusts. The merger of the two regimes was actually expected once these were aligned in a phased manner in earlier years. The proposed reintroduction of a block assessment procedure for search cases and changes to the re-assessment regime suggests a flip-flop approach on the side of the Government as a few years back the block system was done away with and such assessments were made a part of the new 147/148 regime. The rationalization and simplification of the capital gain tax regime, the tax deducted at source rates, proposed increase in limit of remuneration to working partners and proposal to remove imposition of Equalisation Levy is a welcome step.

The proposal to introduce the Vivad se Vishwas Scheme once again will provide much needed certainty and augment the Government exchequer. The proposal to allow the CIT(A) to set aside the assessments which have been completed u/s 144 will certainly help to speed up the pending litigation. Another significant change is to remove prosecution in cases of delay in deposit of TDS as long as the tax has been deposited till the filing of the withholding tax return.

A couple of amendments which will not go down well with the taxpayers are the proposal to impose tax in the hands of the shareholders in case of buy back of shares and the removal of indexation benefit on the transfer of property. While the amendment to the buyback regime is proposed ostensibly to align the same with the dividend taxation regime but the proposed amendment to remove the indexation benefit is neither simplification nor rationalization. This proposal requires a reconsideration by the Government.

From a direct tax perspective, the budget is focussed on better dispute management, providing relief in areas of complexity and balancing all of it with widening of tax base in certain areas.

1. Better dispute management Vivad Se Vishwas 2.0 and Increase in threshold for appeals will go a long way in reducing litigation. Further, reducing the re-assessment period from 10 years to 5 years will also instill investor confidence and encourage wider equity participation

2. Relief in areas of complexity Doing away with angel tax is a big relief for India Inc. Abolishing Equalisation Levy will also go a long way in instilling investor confidence. Reducing long-term capital gains to 12.50% from the existing rate of 20% will also encourage a lot of capital transactions especially in the real estate sector

3. Widening Tax Base All the benefits are sought to be balanced by certain measures to widen the tax base. Increase in STT rates for Derivatives to 0.1% and futures to 0.02% may not go well with investors. Further, increase in capital gains for listed equity instruments to 12.5% will leave investors dejected. Proposing to tax buy-back proceeds as dividend may also pose challenges as buy-back route is opted not only for profit distribution but also for internal re-structuring.

The proposed amendments to the GST law in Budget 2024 are largely to give effect to the recommendations made by the GST Council in 53rd meeting.